By: Iris An

Lazada, the online shopping site owned by the Chinese tech company Alibaba, is struggling to maintain its role as the leading ecommerce firm in Southeast Asia.

With a population of 670 million and over 400 million online users, Southeast Asia is one of the world’s fastest growing internet markets. The region enjoys some of the highest rates of internet adoption, the longest hours online per capita, the largest youth group, and an active local social media industry.

Last year, Southeast Asian countries received more than 40 million new Internet users, with the overall online economy hitting $105 billion and e-commerce exceeding $62 billion, a 63% increase from last year. As covid-19 prompted stuck-at-home consumers to go online for shopping and entertainment, the pandemic catalyzed a permanent and massive digital adoption, just like how the SARS pandemic in 2003 gave a boost to the giant Chinese online shopper Taobao.

The Central business district (CBD) in Singapore (Google Images)

As the largest Internet online industry, ecommerce in Southeast Asia has its own attractions. Since the 2010s, there were once more than 60 online shopping sites competing in this battlefield, including Amazon and eBay, who are yet to make any significant progress.

A few years later, Lazada and Shopee seem to be the final victors.

Lazada is a Singaporean multinational technology company now owned by the Chinese tech company Alibaba after its acquisition in 2016. Interestingly, Shopee’s parent company is the Singapore-based Sea Group, whose largest shareholder is none other than Tencent, Alibaba’s rival in China.

A leading e-commerce firm since 2012, Lazada has more than 70 million customers in the region and a dominant presence across six countries—Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam. But this advantage did not last long.

Lazada and Shopee

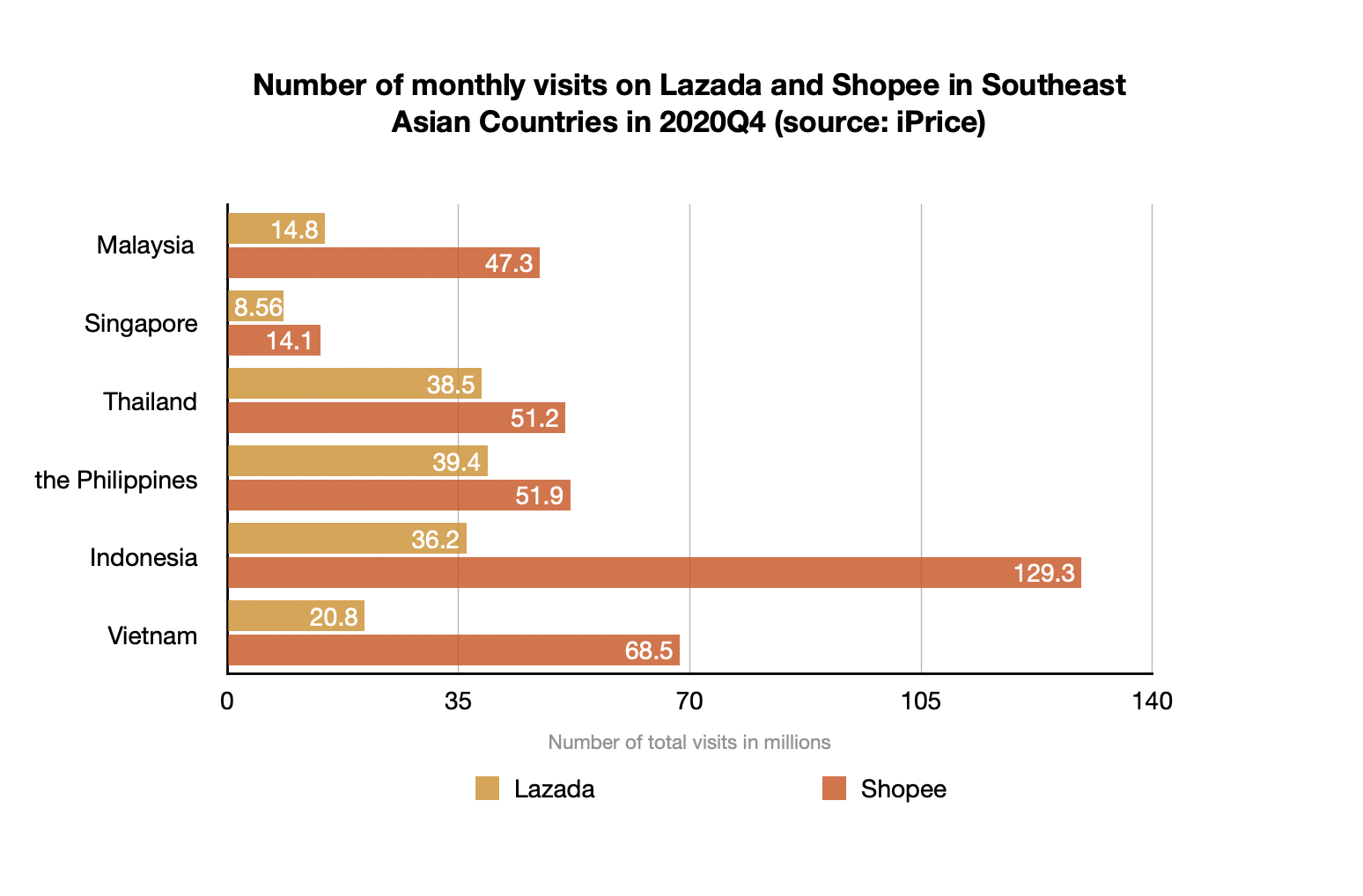

According to the iPrice report, in 2019, Shopee overtook Lazada as the largest ecommerce firm in Southeast Asia, surpassing it in total downloads, monthly active users (MAU) and user retention rate. In May 2020, Shopee was downloaded more often in the six countries in which both companies operate: Indonesia, Malaysia, Philippines, Thailand, Vietnam and Singapore. In the third quarter of 2020, App Annie ranked Shopee first in total downloads, monthly active users, and monthly app hours by Android users in Southeast Asia, and Shopee came second in total global downloads of shopping apps.

From the beginning, Shopee’s success is hard to explain. Founded in Singapore, it was part of Sea’s ecommerce matrix and was way smaller than Lazada in 2015. However, in the following years from 2016 to 2019, Shopee gradually expanded its business to Malaysia, Thailand, Taiwan, China and Indonesia. Owing to Shopee, Sea sees tremendous growth in e-commerce revenue: from $17.7 million in 2016 to $820 million in 2019, the compound annual growth rate is 359%.

What explains Shopee’s rapid growth in Southeast Asia?

As Liu Jianghong, the Head of Cross Border eCommerce at Shopee, said to the media, apart from catching up with the rapid development of the local e-commerce industry, localization is Shopee’s winning formula.

Market segments in Southeast Asia are vastly diversified. Except for Singapore, the other five countries in Southeast Asia are largely underdeveloped, with distinctive demographics, religions, and consumption habits. Even infrastructure conditions like transportation and internet popularity differs greatly. Vehicles in Indonesia, Thailand, Singapore and Malaysia drive on the left, while Vietnamese and the Filipinos drive on the right; and in the Philippines, more than 100 million people are scattered on more than 7,000 small islands.

Therefore, in Southeast Asia, products need to be divided into smaller, more defined categories. Take online clothing shops as an example, European and American brands are more welcomed by Singaporean consumers, while the Philippines is more influenced by Japanese and Korean fashion.

Similar to the giant Chinese ecommerce platform Taobao, Shopee adopts the C2C model, where all types of commerce are done between private individuals. In a market like Southeast Asia, a C2C model allows local consumers to interact and trade with one another. It is therefore more responsive and penetrative than the B2B model taken by Lazada, which involves businesses purchasing goods and services from each other.

Besides setting up a local team to serve its seller partners in different markets, Shopee also develops customized standalone mobile apps for different markets. For example, addressing Indonesia’s daily traffic jams in rush hours, Shopee Indonesia App launched Shopee Shake, a simple game where customers can shake their phones to win coins for future discounts.

Initially, this kind of in-app entertainment feature was a marketing strategy practiced firstly by Lazada, who followed the footsteps of its parent company, Alibaba.

In June 2019, Lazada launched “Laz Live” in Thailand, the Philippines, and Malaysia. Laz Live is a livestreaming function that helps sellers to invite hosts to conduct live streaming shows. This omni-channeled feature enabled sellers to engage with their customers face to face and to replicate the in-store shopping experience.

Unfortunately for Lazada, in the same exact month, Shopee rolled out “Shopee Live,” and covered the three countries Lazada already occupied plus Singapore.

On live streams, Shopee foregrounds localization as its top marketing strategy. While Lazada went into inviting both local and overseas artists, celebrities, and influencers as hosts, Shopee invites only celebrities but also approaches micro influencers such as local university students. While celebrities secured a high view count, traffic simply leverages the hosts’ popularity. On the other hand, the less distant icons increased the familiarity of the app to users, and allowed them to associate the app as something closer to their hearts. Shopee Live was extremely effective, as sellers and brands saw a 75% surge in sales after they participated in the live streaming sessions.

Taking a step further, Shopee launched ‘Shopee Quiz,” an interactive game show incorporated as a section in Shopee Live. The winners in the quiz get “Shopee Coins,” and multiple gifted products from participating brands. To attract more traffic streams, it also opened group games and competitions.

To get their name out quickly, Shopee also invested heavily in celebrity marketing, with big targeted endorsements from popular stars in various markets. In the Indonesian and Philippine markets, it signed Korean girl group BlackPink and the national treasure and world boxing champion Manny Pacquiao as spokespeople and Double 11 brand ambassador respectively. The company even named the football icon Cristiano Ronaldo as its global spokesperson.

Korean girl group BlackPink as Shopee’s spokesperson in Indonesia for its 12.12 promotion (Google Images)

In terms of human resources, Shopee is more stable than Lazada.

Alibaba has always viewed Lazada as an engine for the group’s globalization strategy. Since Alibaba took a stake in Lazada in 2016, it bought up its shareholding all the way to about 90% for higher involvement in Lazada’s business, bringing technical teams from China to reconfigure and upgrade Lazada’s systems, with a handful of people from Alibaba and mid- to senior-level talent stationed in parallel.

But reality proves more complex than a straightforward task to replicate the Chinese giant’s huge success at home across south-east Asia. The five years of Alibaba holding Lazada saw four different CEOs; some of the employees dispatched from China could not integrate into Lazada and were soon transferred back to China. Behind the frequent management changes, Lazada is challenged by internal instability and the increasingly fierce external competition from its rivals. Wary south-east Asian consumers consider Lazada a foreign company, first German and then Chinese, in comparison to Shopee’s local hiring programs.

When the coronavirus crisis hit Southeast Asia in early 2020, countries across the region implemented different degrees of blockade and quarantine measures. Lazada was unable to meet the demand and had to restrict supply and to reduce the range of goods. In comparison, Shopee benefited from the pandemic, showing continuous growth in terms of DAU (daily activity), order volume, and ARPU (single user contribution value). For example, in Singapore, where Lazada had restricted online orders, Shopee’s web visits jumped 82% during the 2nd quarter of 2020. By the end of 2020, Lazada was far behind. According to SimilarWeb, Shopee and Lazada‘s monthly visits in February 2021 were 116.8M and 32.7M respectively. In the two largest markets, Indonesia and Vietnam, Shopee’s monthly visits even exceeded 4 and 3 times that of Lazada.

The competition has yet to reach an end. With its recent restructuring efforts and support from Alibaba’s logistic technology, Lazada is maintaining its presence in Southeast Asia.

As the battle looks likely to become fiercer, it is also an expensive one. After at least $4bn injected, Lazada has become one of Alibaba’s costliest overseas ventures. In 2020, Alibaba described Lazada in its annual report as having “a negative effect on our financial results at least in the short term.”

Shopee experiences a similar situation. In 2019, the Adjusted EBITDA (earnings before taxes, interest, depreciation and amortization) of the e-commerce business was negative $1 billion, which was just enough to spend the positive $1 billion Adjusted EBITDA of Sea’s cash cow, the gaming business.

In the long run, raging costs are a common obstacle faced by all online shopping businesses. As companies like Amazon and Alibaba have demonstrated in their respective native markets, as long as one achieves economies of scale, profitability can be quickly improved by squeezing costs. Will this success formula be rewritten in Southeast Asia?