By: Rohan Upadhyay

America can’t catch a break with COVID-19.

People stay home to avoid getting sick, so they can’t pay the bills and risk getting evicted. If people can’t stay home, then they’re more at risk of getting infected. And even protesting to change eviction policies puts people at risk of catching COVID-19 as people gather in large groups.

On top of that, when people get laid off, they lose their health insurance. Just what you need in a pandemic.

Healthcare is tied to Employment — Bad Idea

In the US, people mainly get health insurance through their employers.

If you lose your job, you lose your health insurance. If you’re in between jobs, you’re not covered.

Normally, this isn’t too noticeable. But this year, we saw a recession with over a million jobless claims each week.

As I said, businesses lay people off because the economy suffers, and then people lose their insurance, which they need in a pandemic.

The question is: how many people lost insurance due to COVID-19? Let’s look at a few sources:

- Robert Wood Johnson Foundation/Urban Institute — In July, it was projected that by December, 10.1 million people could lose insurance. However, most of them may find another option. For example, many people may enroll in Medicaid. Unfortunately, the process of switching insurance is cumbersome, and it means that you’re temporarily left uninsured (good luck if you get sick during that gap). Ultimately, 3.5 million could be left uninsured.

- Families USA (D.C. Nonprofit) — They determined that 5.4 million people lost their health insurance due to job losses from February to May.

- Kaiser Family Foundation (KFF) — Not everyone has their own insurance. People are often “dependents” — for example, children depend on their parents for insurance. KFF considered this and estimated that 27 million lost health insurance as of May 2020. They also reported that by January 2021 — when unemployment insurance will end for many people — 17 million will be eligible for Medicaid. We could see a wave of people enroll in Medicaid, which could overburden the public health system.

It’s possible that these studies underestimate the uninsured count — there may not be perfect records of jobless claims. Maybe they’re overestimating (they may have miscounted people who found replacement insurance). But there seems to be evidence that we’ve got an insurance crisis on our hands.

That means that people may be less likely to get treatment if they’re sick, fueling the pandemic. If they do see a doctor, then they’ll struggle with medical bills — exacerbating the recession.

Finding Alternate Insurance

We should discuss the fact that not all insurance is employer-based. For example, people in need can get government coverage through Medicaid. Obamacare gives subsidies to people who struggle to pay. There’s also COBRA insurance. Let’s look at each of these.

COBRA (Consolidated Omnibus Budget Reconciliation Act)

The first line of defense against losing employer-based insurance is COBRA. It lets people continue to receive coverage through their employers even after losing their job.

Here’s how it works: if you lose your job (or are forced to work part-time), then you can sign up for COBRA within 60 days. You’ll get the same coverage that you had for 18–36 months. However, you have to pay much more.

Normally, your employer pays most of your health insurance premiums (the periodic fees that your insurance company takes). Maybe your employer pays 80% and you pay 20%, for example. However, if you’re laid-off and you enroll in COBRA, you have to pay the whole amount of the premiums.

The idea is to have an organized system to help people continue their coverage even after losing their job — they don’t have to worry about finding a job immediately to get health insurance, as this option is readily available (*only for companies with over 20 employees*). But businesses won’t pay your insurance after they get rid of you, so you take on the burden.

It’s not ideal, and having your bills go up that much during a pandemic and recession is the last thing you want to think about.

But COBRA is really meant to be a transition state for a brief time, not a long-term solution for someone who’s lost their job. So what’s the next option?

Obamacare Marketplaces

The Affordable Care Act (Obamacare) established a marketplace for health insurance. It’s known as healthcare.gov.

There are loads of private insurance plans in this marketplace. If someone is in between jobs, then they can enroll in healthcare.gov to get help in finding a plan. Obamacare also did the following:

- Gave people subsidies to help pay for the plans.

- Reimbursed insurance companies who are required to offer cheaper insurance plans in this marketplace.

- Created outreach programs to make people aware of how to sign up.

This national market place was created to slash prices — companies in this market place were required to offer cheaper plans, and more competition would also reduce prices. It was also intended to give people a quick way to find insurance while in between jobs.

However, the Trump administration cut reimbursements to the companies, along with outreach funding. Now, insurance companies may push back against providing cheaper plans, and it could be harder for people to sign up with healthcare.gov.

However, there is one more option that we haven’t discussed…

Medicaid

If you lose your job and struggle financially, you can qualify for Medicaid.

But enrolling in Medicaid can take 45–90 days. That’s a giant window to be left uncovered.

Another issue is that — with so many people losing insurance — we could see a wave of people enroll in Medicaid. As stated before, the Kaiser Family Foundation (KFF) found that 17 million people could be eligible for Medicaid by January. As people move from private insurance to Medicaid, Medicaid could become overburdened with sick people if COVID-19 gets worse.

Also, KFF reported that 6 million people could become eligible for Obamacare subsidies. Furthermore, KFF projected a “coverage gap” of 1.9 million Americans. Basically, these are people who make too much to qualify for Medicaid, but not enough to qualify for Obamacare subsidies.

Okay, that’s weird — how does that happen?

So, one part of Obamacare was the “Medicaid expansion.” When Obamacare was passed, many states expanded Medicaid by increasing how much money you can make before you qualify for Medicaid — you don’t have to be *as* poor to qualify for Medicaid now in many states. With that, the Obamacare marketplace subsidies are only offered to people who make more than the Medicaid threshold.

However, some states didn’t expand Medicaid, so they’re still at the lower (more strict) threshold. In these states, there’s a gap between the Medicaid upper threshold and the marketplace subsidies lower-threshold. This coverage gap could leave 1.9 million people uninsured by January.

Too Many Holes — We Need Universal Healthcare

We have a system in which people lose their insurance if they get fired in a recession, which they need because we’re in a global health pandemic.

From there, people can get (1) COBRA insurance, which is pricey. Alternatively, they can go to the (2) ACA marketplace, which Trump has undermined. Finally, they can (3) enroll in Medicaid, which will leave them uncovered for several weeks and cause Medicaid to be overburdened with too many sick people.

The problem is that our system is fragmented. We have all these programs with separate qualifications that don’t always line up, and that makes transitioning cumbersome. It also means that if people can’t access one system (like employer-based insurance right now), then they’ll flock to another (like Medicaid) overburdening it with too many sick people (like right now with the COVID-19).

If we had one universal system that covered everyone, these problems could go away.

If there was one mechanism that everyone used, then people would always be covered, costs would be constant, and people wouldn’t have to worry about switching between insurance programs with cumbersome enrollment. The risk would also be spread evenly over everybody.

During a pandemic, people can’t waste time figuring out insurance. People should have coverage when they need it — that helps people get treatment faster, slowing the spread of the virus and keeping the pandemic at bay. Having a single, universal system can help.

For example, in Canada, Australia, and many EU countries, the government covers everyone. All residents are automatically enrolled, and your tax dollars constantly fund your insurance so that you never think about enrolling or switching insurance. This is known as a “single-payer” system (the government being the ‘single-insurer’).

Alternatively, countries like Switzerland also have universal healthcare, but they do it by regulating private insurance heavily. People are mandated to buy insurance, private insurers are required to cover various needs, and insurance costs are subsidized. People can buy insurance from whomever they want (increasing competition and decreasing prices), unlike here where your employer dictates your insurance provider.

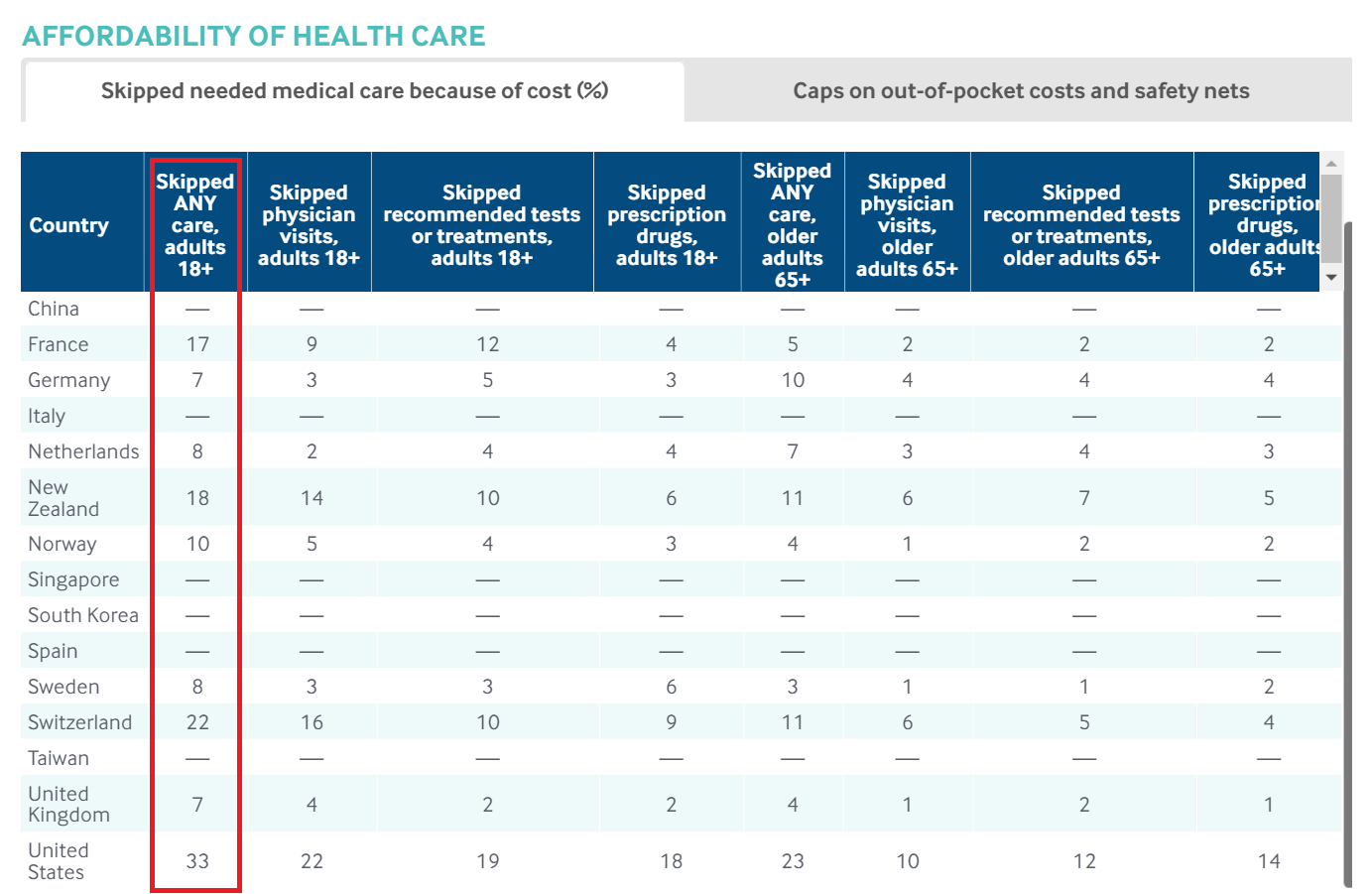

The effects of US healthcare on its constituents are evident. As of April (which is admittedly early), 33% of Americans skipped medical care due to costs. That’s higher than in other countries. That could be because countries with universal healthcare have mechanisms built in to reduce costs more so than the US, so cost isn’t as big of an issue. Thus, a universal system could bring down costs and make the crisis easier to manage for the government and for individuals.

33% of Americans “skipped ANY care” as opposed to 22% of Swiss people and between 7-18% of people in other countries. Canada and Australia (not shown) are 16% and 14%, respectively. Source: Commonwealth Fund.

The point is that – while no system is perfect – there are government-based and market-based ways to reach universal coverage. These are ideas that we’re not discussing enough. A universal system, whatever it looks like, would help us manage COVID-19 in an orderly way, unlike our (relatively) disorganized approach.

People are encountering problems due to COVID-19 that are not immediately obvious. Let’s not forget that.